The Greek Crisis: A Debt Trap Conspired by Europe and the U.S.

The Beginning: A Transaction

Greece, the ancientest country in the European Union. In the 80s, this Orthodox nation, constantly in crisis and foreign domination, finally joined the rational, prosperous and civilized European family. Membership in the EU seemed like an ecstasy, from the bottom workers and peasants to the capitalists and offshore elites, as if Greece had finally returned to its rightful place in history after the oppression of the Ottomans and the chaos of the modern era.

Shortly after the end of the Cold War, the Greek government, together with the European Commission, put forward a proposal: they wanted to go one step further and join the eurozone by giving up the management of their chaotic currency. What country wouldn’t admire a strong euro? Every Greek worker at the end of a hard day’s work would remember that the currency in their pockets is the same as the currency in the hands of German business executives and French politicians and businessmen. Trade with Germany would flow freely, Protestant and Catholic tourists would flock to Athens and Crete because of the history of ancient Greece, and most importantly, the leaders who made it possible would go down in history as heroes along with Heracles and Odysseus.

The Greek Debt Crisis, an international political metaphorical drama set in contemporary Greece, has a classic beginning: Hubris (arrogance) sets Greece on a path of self-destruction as an aging hero. In order to join the Eurozone, the Greek government relied on a financial forgery package provided by Goldman Sachs to cover its public debt and keep the state’s budget deficit below the 3% of GDP required by the Maastricht Treaty.

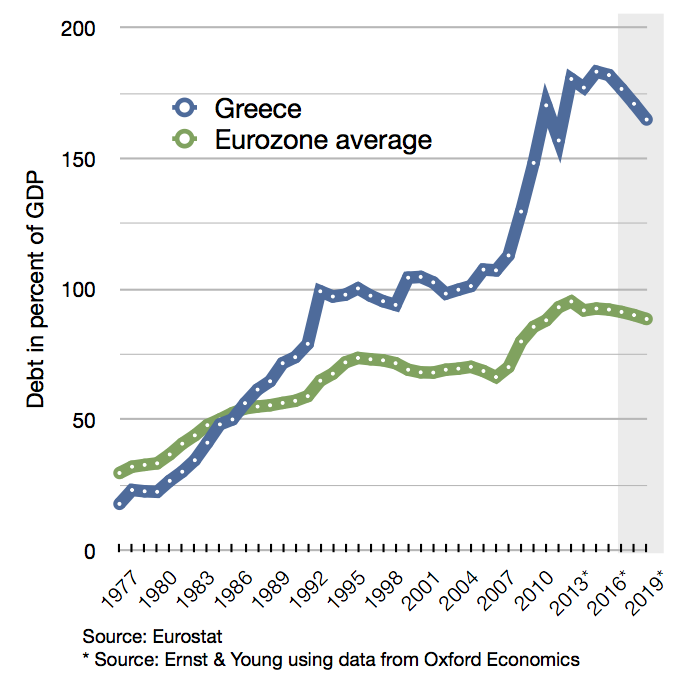

Although the Greek government hoped that after joining the European Union the Greek economy would be able to regain its post-war glory of the 1970s, and they tried everything from welfare expansion to Keynesian policies, they were unable to reverse the economic decline. The repeated devaluation of the currency did not improve the situation of the secondary sector and the employment rate, but became a catalyst for debt. From Greece’s entry into the European Union in the early 1980s until the eve of the abandonment of its own currency, Greece’s debt as a percentage of GDP rose from 23% to a staggering 103%.

Goldman Sachs, which provided the previous Greek government with the counterfeiting scheme of cross-currency swaps, received a commission of up to $300 million, which was charged as a percentage of the amount of the transaction; at the same time, Goldman Sachs purchased a 20-year, €1 billion credit default insurance (CDS) and shorted collateralized debt obligations (CDOs) on the other end of the deal, which means that, if Greece falls into a crisis in the future, Goldman Sachs will not lose money but will be able to make another big profit. It could make another big profit.

What works is always going to work again and again. Right after the currency swap agreement, the Greek government and Goldman Sachs signed another long-term bond interest rate swap agreement. But just three months after this new agreement came into effect, the 9/11 attacks occurred, bond market yields fell sharply, even if Goldman Sachs modified the repayment terms, Greece still suffered a loss of 5.1 billion euros. The administrator of the Greek debt received a warning from Goldman Sachs to cancel the transaction and was unable to go to the market to test the offer made by Goldman Sachs, which had not suffered any loss due to its previous hedging strategy. The nuclear button to expose the scandal was in the hands of Wall Street, and the Greek government lived off their mercy.

What does Greece’s accession to the eurozone mean to the masters of Europe? After unification, Germany urgently needs to expand its economic influence through the eurozone to offset the impact of the appreciation of the mark on exports; Greece’s accession to the eurozone can enhance the coverage of the euro as an international currency, especially favorable to the export of German commodities denominated in euros - made in Germany in Eastern Europe’s industrial layout of another puzzle; in addition, the single market of the EU will aggravate the hollowing out of Greek industry, but this precisely meets the core countries such as Germany by means of the core countries through the hollowing out of the Greek industry. In addition, the EU single market will aggravate the hollowing out of Greek industry, but this precisely satisfies the purpose of Germany and other core countries to exploit southern European countries through trade surpluses. The EU’s statistical institutes already knew after the 2004 survey that Greece had taken some unorthodox measures to adjust its debt figures, but they unspokenly only expressed their concern and did not carry out more detailed checks - after all, Germany is one of the most active players in this lending speculation game, and there is no reason to release information that would shake the value of these bonds. After all, Germany is one of the most active players in this game of lending speculation, and there is no reason why the release of news that would destabilize the asset value of these bonds would be a drain on the purse strings.

A Turn: A Conqueror Known as Fiscal Discipline

The fundamental flaws in the design of the eurozone, especially the lack of a fiscal union and banking union, made the eurozone fragile in the face of the financial crisis in 2008 and left the non-core countries without information and voice in critical moments. 2008 financial crisis, French Finance Minister Delors wanted to use the crisis to push for the establishment of a fiscal union, while German Finance Minister Schaeuble advocated maintaining stability in the eurozone through strict fiscal discipline and a possible “Greek exit from the eurozone”. Germany’s finance minister Schaeuble advocates strict fiscal discipline and a possible “Greek exit” from the eurozone to maintain eurozone stability. The Germans were conservative and wanted to limit the size of their debt, while the French were radical and wanted to realize the commonization of debt, so that the Germans would bleed heavily. In the end, Europe chose to maintain the status quo of the eurozone through massive austerity. But the problems remained, and even became more serious. Fiscal discipline is loose, exchange of information is blocked by interest groups, and voice is monopolized. … Above all, deficit countries such as Greece and Italy remain in the eurozone: on the one hand, Germany has failed to change the fragility of the euro; on the other hand, since it has failed to change the fragility of the euro, it has eternized it, and, at the critical moment, it has driven out the eurozone as a means of threatening to force the Germans to leave the region. On the other hand, having failed to change the fragility of the euro, Germany has eternalized it, and at critical moments has used the expulsion from the eurozone as a blackmail to force countries like Greece and Italy to compromise.

The Germans thought that they could restrain the expansion of the European countries’ economic landscapes through the mandatory austerity policy, so that Germany, the number one industrial power in Europe, could strengthen itself and at the same time stabilize the core industries of the deficit countries, led by France,from being jeopardized. This seems reasonable: the specificity of each industry after the Second World War has led to the specificity of the interest groups formed around them. Under the EU system, these industries are bound to be carried by countries adopting diverse economic and social policies and coordinated by the EU political and business circles, so that no European country other than the USSR can monopolize all of the industry’s capital. However, contrary to expectations, the euro did not become a tool for the French to build a fiscal union, nor did it become a straw for the German political and business sectors. Instead, it led to a long-term underinvestment in Europe after the financial crisis in 2008. At this time in the 21st century, the German- led austerity policy is more than a bitter meaning, because the European investment want to make money in the final analysis need to get the approval of the Americans, even if the bond issue is also very difficult to ensure that the return will only be more and more deeper into. In this regard, the German-led central bank and the French Ministry of Finance of the fiscal discipline of the tug-of-war has changed the flavor, no party can really realize the independence and autonomy of Europe, the EU political and business elites on behalf of the interests of not the interests of the Germans, not the interests of the French, but the interests of the Americans and the offshore elites.

Perhaps because the three major rating agencies in the United States kept downgrading the credit rating of Greek finances, or perhaps because the Wall Street elites who had been informed of the insider information spread the word by word of mouth, Greek bonds were downgraded to junk rating in April 2010, and the crisis officially broke out.

Since 2010, the European Commission, the European Central Bank, and the IMF have been providing bailout loans to Greece, but with harsh austerity policies attached, including cuts in public spending such as pensions, massive privatization, and tax increases. The core of this program is debt rollover rather than write-downs, depriving Greece of autonomous control over its finances; shrinking Greece’s GDP and the size of its business and industry, driving up the poverty and unemployment rates; and implementing neoliberal structural reforms, weakening workers’ bargaining power, driving down wages, forcing the sale of domestic assets, and driving up value-added taxes while conniving at the oligarchs.

These bailout loans will not become real investments and relief for the people, but will go directly into the pockets of German and French creditors and banks. Germany itself was the biggest creditor of Greece. The Germanic people, who emphasized discipline, refused to write down their debts, and forced Greece to pay back the loss of private capital by impoverishing its entire population. Not only that, but morally, Merkel wrapped this package in the “Greek laziness theory” to cover up the flaws of the euro system - a modern country with an unemployment rate of 20% must be a national problem. Together with the Americans, the German capital in Greece in crisis began a rapid horse race, not only to reduce the scale of the Greek industrial services, but also to control the remaining key industries and infrastructure, the already small profits plundered into their own pockets. The poorer the Greeks were, the poorer they became, and the poorer they became, the poorer they could not make their payments, so they had to sell everything they had to pay the interest. These are real debt traps compared to the Belt and Road Initiative’s real-life debts for power and transportation infrastructure and schools and hospitals.

The previous pitfalls of the Eurozone have now become weapons of arbitrage for the core EU countries, driving German industrial capital, British, French and American financial capital and EU technocrats to form a community of interest that will take advantage of the debt crisis to complete the economic colonization of southern Europe. The cage of austerity has kept Germany’s energy-consuming, gigantic old car running in an extremely inefficient way, inhibiting the development of new industries and deficit countries, and is now beginning to bare its destructive fangs against Greece, the most disadvantaged of all countries.

Wrap: Superhero Syriza

In January 2015, the Radical Left Alliance, a left-wing Greek party that supported anti-austerity policies and claimed to be able to resist the Brussels, Berlin, Frankfurt axis, came to power. Prime Minister Alexis Tsipras led all the Greeks to wield their slim fists against the US, Britain, France and Germany on Mount Olympus. The main demands of the Radical Left were threefold: 1) to write down, not roll over, the debt; 2) to end privatization and increase public investment; and 3) to combat tax evasion and reinstate progressive taxation. This radical program has been welcomed by the public and has been successfully adopted in the referendum as the national strategy for the next phase of Greece’s development.

In 2012, the Radical Left chose the slogan “exit from the eurozone” for their election campaign, which did not win them majority support. As an alternative, these three demands are the result of a compromise with reality. It must be said, however, that these three demands, which could be called a “minimum program”, do not lose their progressive significance in the context of a compromise, as was first seen in the outcry of many EU establishment analysts in January ‘15 when they said. Debt write-downs - which, incidentally, are a statutory power of the Greek finance minister - will lead to a shrinking or even zeroing out of bond assets held by Germany and the ECB, and Greece will no longer need to overspend on its own future; the end of privatization and the crackdown on oligarchs will allow the Greek state to The end of privatization and the crackdown on oligarchs will allow the Greek state to take back control of key livelihoods and infrastructure, and to stop the boisterous sale of natural resources and land.

The ECB’s response was drastic. First, they cut off liquidity, no longer allowing the Greek central bank to use Greek debt papers as collateral - it must now use the ECB’s emergency liquidity assistance to fund banks in Greece and assume all the risk of borrowing, rather than allowing the rest of the eurozone to share the risk. The new Greek government’s response was simpler and more direct. The prime minister relied on his domestic reputation to appoint Finance Minister Varoufakis, whose aggressive bond-freezing program sent Europe’s well-informed lobby and analysts into a panic. As Varoufakis himself put it: if the bank squeezes you, you squeeze back.

The plan to freeze the payment of the bonds was called by Varoufakis himself “the vent of the Death Star”, “the seam in the armor”. It was a crazy decision, but one that was made in the blind spot of the Western bourgeois elite. The debt of the southern European countries is a deadlock that the German political and business community has been struggling with for a long time and has not been able to solve. Italy’s public debt has reached 2.2 trillion euros in 15 years, which is already 132% of GDP. Schaeuble, the finance minister, who has been a strong advocate of downsizing the eurozone, has been at loggerheads with Merkel on this issue, and has now been hand-delivered by Merkel herself. As long as Greece’s debt is effectively written down through a freeze at this point, it will be extremely difficult for the ECB to deal with Italy’s debt, which is a much bigger player in Europe than tiny Greece.

Politically, Tsipras’ government and he himself are firmly in the left-wing discourse. The referendum showed that more than 60% of the Greek public did not want to accept the EU’s fiscal program as a thirst quencher, and after the speech in the European Parliament, the left-wing factions within the EU have gradually shifted to politically support the Greek radical- left coalition in the struggle. This is a very big force.

The resistance of the Radical Left Alliance is just and effective in reality. In contemporary society, the power of a weak state that has been repeatedly exploited by a transnational elite and hollowed out industrially is limited, but the Radical Left has, after all, gained substantial control over a piece of land, over the state apparatus and over the leadership of the masses who are willing to rise up and fight in the midst of the oppression. They have entered the deep waters of practice, the realm where only a few radical left-wing parties have set foot for more than a hundred years.

They found themselves in a situation of isolation similar to that of many South American socialist regimes, with a European core on the one side and the United States and its proxies in full force on the other. There is no internationalism that can be their foreign aid, not even a neutral country that can provide trade opportunities in the midst of the blockade. In short, if these Commie scum, treated as lambs to be slaughtered by international financial capital, tried to rebel against the feudal lords, they would surely be slaughtered and eaten up.

Ending

At this point in history, the only road left before them is to fight. The Greeks had the capital and the means to bring down the fragile system of the European Union, and even if they couldn’t, they could still tighten their belts and live in misery if they were willing to take the path of radicalization.

Unfortunately, the struggle of the Radical Left Alliance failed in the face of the EU’s blockade and the paucity of international support. On the day of the referendum, Tsipras went soft and decided to sign a third memorandum of understanding. The program of economic reforms was reintroduced, and the Greek people, united in their resistance, were taken by bourgeois academics as an example of communist “residue” and populist catastrophe. The Radical Left was then in a state of denunciation. It introduced some limited reforms, but in the end it failed to touch the global capitalist system that arbitrage and cause the most damage. In the latter part of its reign, this improvised party was forced to paradoxically implement measures it did not want to and should not have taken, resulting in its subsequent fragmentation and rapid demise.

Internationally, the struggle of the Radical Left Alliance was not universally supported, but the failure of the movement was still meaningful. It exposed the vulnerability of the rigid and brain-dead EU system in the face of a mere financial uncertainty, and used the ultra-high unemployment and poverty rates in Greece after the signing of the Third Round of the Memorandum of Understanding to reveal the dirty face of the American, German and French bourgeoisie, which is hidden under the umbrella of European solidarity and eurocentrism. It should serve as a warning for the poor and weak countries in Europe to see that their right to survival and development has been placed under the interests of Germany and France, and that their fate is no better than that of the countries in South America that have been seized by the CIA, and that the only choice is to join hands with the international proletariat and the global third world in breaking through the cage created by this global capitalist booty-sharing system, which is typified by the eurozone.

This unsuccessful struggle shows even more that the necessary condition for proletarian dictatorship is not only to seize power, but also to realistically maintain its existence under the pressure of transnational capital and offshore elites, to find a breakthrough in the global capitalist system, and above all, to take a courageous step in practice, to utilize this breakthrough to give a counter-attack, instead of only verbally threatening, but not daring to do so at all. It is not just a matter of paying lip service to blackmail, but not daring to change the status quo beyond what the masters allow, let alone making sacrifices for their own people or even for members of their own organizations.

What is needed is definitely not the lip-service unity of those radical leftist groups in Europe, definitely not the recitation of left-wing theories and scriptures, not the pretentious visits and investigations and writings, and not the pathological clamouring and tsunamis. What is needed is courage to make sacrifices, realistic organizational mobilization, and solidarity that can withstand blockade sanctions. This article is the beginning of a series. We will publish more analyses and commentaries on colonization and other internal conflicts in the EU in the future.